- September 5, 2025

- Posted by: Melanie Scott

- Category: Market News

Canadian employment shocked this morning with a disappointing 65,500 drop in employed people, following July’s 40,800 decline. This bumped Canada’s unemployment rate up to 7.1%, while it was projected to increase marginally from 6.9% to 7.0%. This marks Canada’s highest unemployment rate since May 2016, excluding the COVID-19 pandemic. The stalled job market adds pressure for BoC rate cuts with the next rate announcement scheduled for Wednesday, September 17th.

The latest U.S. data points to an equally agonizing labour market south of the border. On Thursday, ADP reported non-farm employment rose by 54,000 in August, falling short of expectations for a 73,000 increase and well below July’s 106,000 gain. The U.S. Bureau of Labor Statistics’ report today confirmed a softening labour market, with their non-farm employment number hitting just 22,000 (expected 75,000) with average hourly earnings seen rising 0.3% month over month and the unemployment rate edging higher to 4.3%. Hiring has slowed under the weight of import tariffs and stricter immigration policies, with the government reporting that in July there were more unemployed workers than job openings for the first time since the pandemic. Weekly unemployment claims also ticked higher, rising to 237,000 from 229,000 the week before, and exceeding expectations of 230,000.

Despite the soft labour picture, the American services sector is showing resilience. The ISM Services PMI expanded for a third consecutive month, climbing to 52.0 in August from 50.1 in July, signaling modest but steady growth in U.S. service activity. Meanwhile, trade tensions remain in focus. After the U.S. Court of Appeals ruled that Trump’s reciprocal and fentanyl-related tariffs were illegal, the former president is now seeking support from the Supreme Court to uphold them. The tariffs will remain in place until at least October 14th as the appeal process unfolds.

Canada’s merchandise trade deficit narrowed to C$4.94 billion in July from C$5.98 billion the prior month, driven by stronger exports of crude oil and passenger cars to the U.S. However, the fiscal outlook remains strained. Prime Minister Carney stated on Wednesday that October’s main budget will prioritize austerity and targeted investments, admitting current government spending is unsustainable. Economists remain skeptical of Carney’s pledge to balance the budget within three years, given rising defense costs, weaker tariff revenues, the cancellation of the digital services tax and other tax relief measures.

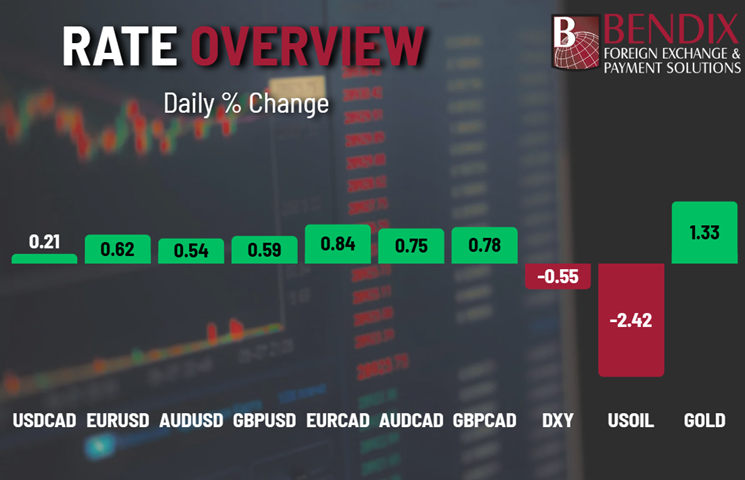

Oil prices dropped more than 6% over the last three days following reports that OPEC+ may consider increasing supply at its meeting this weekend.

Manage your FX risk with confidence—contact Bendix to find out how we can help you stay ahead of market movements.