- June 12, 2025

- Posted by: Melanie Scott

- Category: Market News

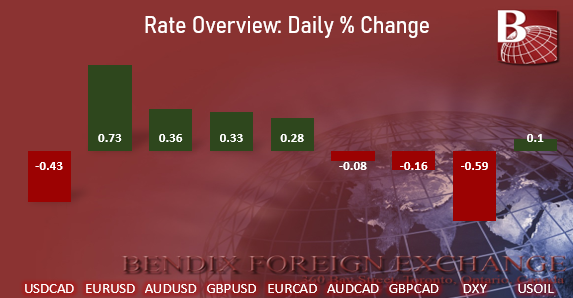

The U.S. dollar continued its slide today, hitting another multi-month low against the Canadian dollar, down 0.43% from yesterday’s close to levels not seen since early October 2024. A string of softer-than-expected U.S. economic data is driving renewed speculation that the Fed could cut rates as early as July. Yesterday’s core CPI surprised to the downside, rising just 0.1% month-over-month versus the 0.3% forecast. That dovish tone was reinforced today by similarly tame PPI data: headline and core PPI both rose only 0.1% in May. Meanwhile, initial jobless claims came in at 248K, above the 242K forecast, extending an upward trend that highlights ongoing cracks the labor market. The Fed will meet next Wednesday when it is widely expected to hold rates steady. With inflation pressures easing and labor market softness mounting, sentiment shifts toward concerns about economic resilience, and market expectations for a July rate cut are rising quickly.

As the July 9 tariff pause expiration date nears, President Trump stated that he intends to send formal letters to trading partners over the next few weeks outlining unilateral tariff levels. At the same time, U.S.-China relations appear to be improving. On Tuesday, both countries announced a framework and implementation plan to reduce trade tensions. Trump expressed support, calling the deal “done,” pending final approval from both him and President Xi. Treasury Secretary Scott Bessent added yesterday that it’s “highly likely” the tariff pause will be extended for countries negotiating “in good faith.” However, the market remains skeptical and investors are turning to safe-haven assets amid rising Middle East tensions and lingering doubts about the durability of the U.S.-China so-called done-deal. The Swiss franc and Japanese yen both jumped sharply today—up 1.04% and 0.52% against the dollar, respectively. Gold is also up 0.96% today.

Across the Atlantic, UK GDP contracted by 0.3% month-over-month, notably worse than the expected -0.1%. This marks the sharpest monthly decline since October 2023. This pushed the pound down to a six-week low against the euro. Meanwhile, the euro surged to its highest level against USD since late 2021. Strength is supported by a more hawkish tone from the ECB, which hinted at a pause in its easing cycle after eurozone inflation returned to its 2% target.

Current Market Conditions: