- July 25, 2025

- Posted by: Melanie Scott

- Category: Market News

U.S. jobless claims came in at 217,000, better than the 227,000 forecast yesterday. However, manufacturing PMI disappointed at 49.5 (vs 52.7 expected), while services surged to 55.2, beating the 53.0 estimate. The U.S. dollar strengthened off the back of this data and this morning continued its gains as President Trump commented on his visit to the Federal Reserve, calling it a “good meeting” with Chair Powell and confirming there’s no plan to fire him. Still, last week’s market reaction to the possibility highlighted just how sensitive investors remain to any hint of political interference at the Fed. An actual dismissal could spark a historic sell-off, with Deutsche Bank estimating a potential 6% drop in the dollar.

As widely anticipated, the ECB held rates at 2.15% after seven straight cuts. ECB President Lagarde described the eurozone economy as resilient, with inflation near target, and dismissed concerns about the disinflationary impact of a stronger euro. She emphasized the ECB remains focused on medium-term inflation expectations, not short-term currency swings. Flash PMI data showed the European private sector economy continued to deteriorate. France’s manufacturing reading came in just under expectations at 48.4, while services matched forecasts at 49.7. In Germany, manufacturing improved from previous 49.0 to 49.2 (vs 49.4 expected), and services edged up to 50.1. The UK showed stronger manufacturing at 48.2, beating estimates, though services disappointed at 51.2 compared to the 52.8 consensus.

In Canada, core retail sales fell 0.2% m/m as expected, while headline retail sales dropped 1.1%, missing both the forecast and prior month’s growth. The Bank of Canada is expected to hold firm at 2.75% next week, with policymakers signaling that any future easing hinges on further weakening in demand and trade clarity. While core inflation remains stubborn, the broader economy shows signs of fragility. The market still expects two rate cuts later this year, most likely kicking off in September, contingent on a sustained slowdown and reduced inflation pressures.

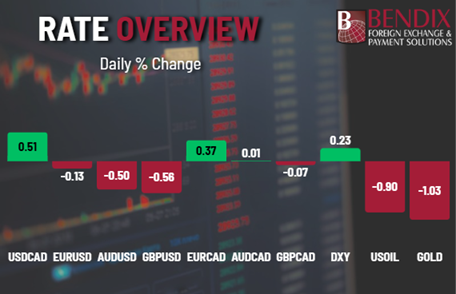

Current Market Conditions:

Take control of your FX exposure and make informed decisions—contact Bendix today to explore tailored solutions for managing currency risk.