- November 28, 2025

- Posted by: Robert Marshall

- Category: Market News

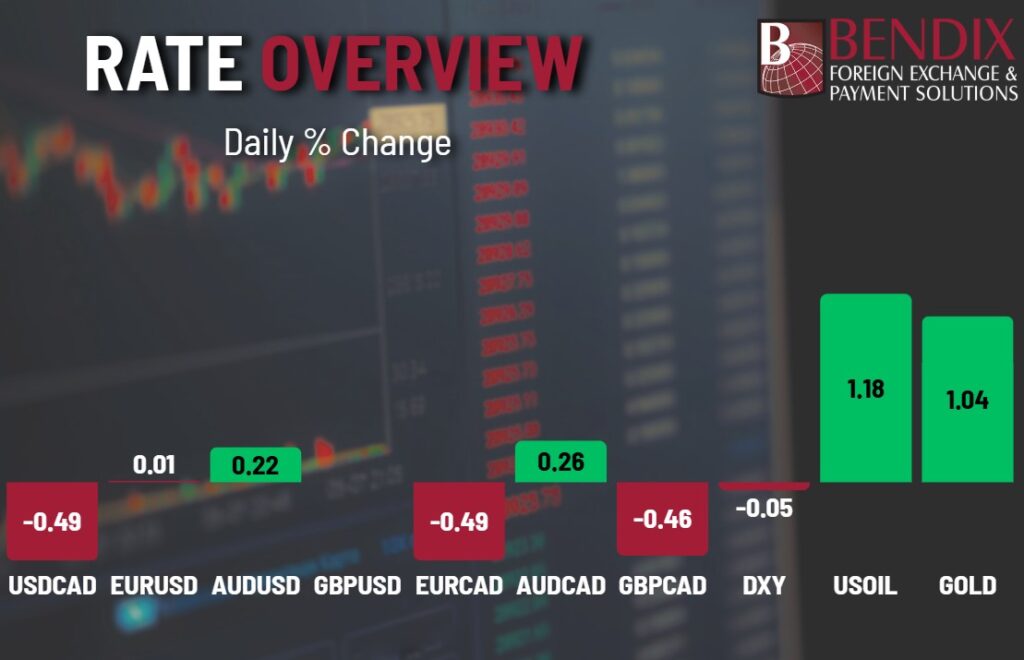

Key takeaway: The U.S. dollar lost ground this week as markets decisively priced a December Fed rate cut, allowing major currencies to recover. CAD underperformed on weak retail data, while JPY intervention risks remain a key market theme.

US Dollar

Expectations for a December Fed cut strengthened significantly, with futures-implied odds now above 80% for a 25 bp move. FOMC minutes highlighted internal divisions, but softer data and dovish commentary pushed the market toward easier policy. The U.S. Dollar Index drifted lower, on track for its biggest weekly fall in four months as investors position for early 2026 cuts.

For corporates, this marks a transition from Q3’s strong-dollar environment toward a more data-dependent backdrop heading into year-end.

Canadian Dollar

CAD remained under pressure following November’s weak retail data: headline sales were flat while core sales declined. USD/CAD held near recent highs as markets price divergent policy paths between central banks. Today’s Q3 GDP release is critical; a downside miss would reinforce CAD’s recent underperformance.

Euro and Sterling

EUR/USD benefitted from softer dollar tone, posting a weekly advance as the market expects the ECB to move more cautiously on cuts than previously priced. Sterling staged a notable rebound, with GBP/USD recording its largest weekly percentage gain since August, helped by improved fiscal sentiment and better risk appetite.

Japanese Yen

After weeks of weakness, the yen recovered as USD/JPY pulled back from recent highs this week. Japanese officials have warned about potential intervention if moves become disorderly, with markets focused on the key technical zone that has drawn repeated official warnings. This creates two-way risk: renewed USD/JPY strength toward prior peaks could trigger policy action, while softer U.S. dollar sentiment supports yen relief.

AUD and NZD

Both outperformed in a weaker-dollar, risk-on environment. NZD jumped to a three-week high on central bank communications. AUD held at elevated levels, supported by the weaker USD and stabilizing global appetite.

Looking Ahead

The next key drivers are:

- Fed decision and U.S. data: With markets heavily priced for a cut, a no-cut signal could trigger sharp USD volatility.

- Canadian GDP: Today’s release will shape Fed-BoC rate differentials, a key CAD driver.

- JPY intervention risk: Any USD/JPY move toward 160 would significantly raise Japanese action probability.

For hedgers and treasurers, adjust ranges rather than chase breakouts, USD is shifting from strength to a balanced, policy-driven regime, while CAD, JPY, GBP, and NZD dynamics are reasserting themselves.

Market conditions as of 11:23 EST