- October 16, 2025

- Posted by: Melanie Scott

- Category: Market News

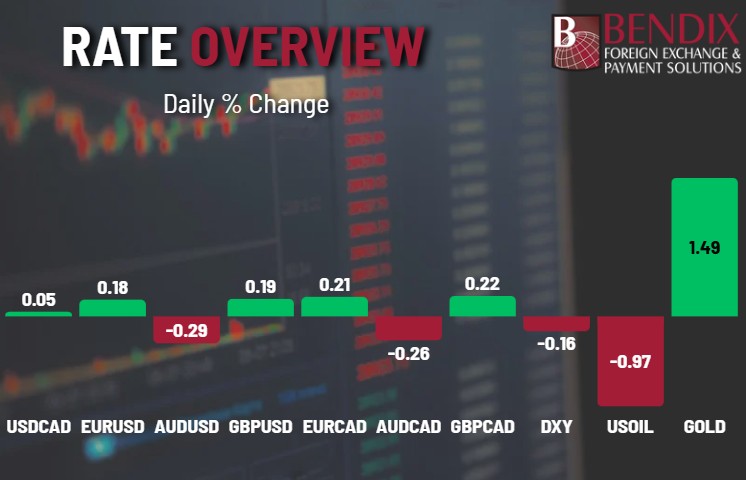

The US Philly Fed Manufacturing Index surprisingly fell negative, posting -12.8, missing forecasts of 8.6 and more than offsetting last month’s 23.5 point increase. While the shipments index eased, it remained positive; new orders showed a modest increase. The employment index edged lower but continued to signal overall gains in hiring.

The US dollar index (DXY) is extending its losing streak to a third consecutive day as renewed U.S.–China trade tensions and dovish comments from the Federal Reserve weighed on sentiment.

In the UK, GDP rose 0.1% month over month in August, matching expectations and rebounding from July’s 0.1% contraction. Production climbed 0.4%, while services stagnated and construction slipped 0.3%. The data suggests a modest recovery, supporting a steady or slightly dovish Bank of England stance amid persistent stagflation pressures.

The euro edged higher against both the USD and CAD after the French government survived a no-confidence vote. Prime Minister Sébastien Lecornu pledged to suspend the pension reform until after the 2027 election, a move seen as sacrificing one of President Macron’s signature achievements to ensure the government’s stability. Attention now turns to the challenging task of passing the 2026 budget through the lower house before year-end.

In Australia, the unemployment rate unexpectedly climbed to 4.5% in September, a four-year high, up from 4.3% previously. The economy added 14,900 jobs, recovering from August’s 11,900 decline but missing forecasts of 20,500. Following the report, markets now price in a 72% probability of a November rate cut, up from around 40% earlier.

Current Market Conditions:

Take control of your FX exposure and make informed decisions. Contact Bendix today to explore tailored solutions for managing currency risk.